Nutanix, Inc. has announced financial results for the first quarter of FY2024. Revenue is up 17.8%, and gross margin is at 84%, although the company made a loss of $11 million for the quarter. Is the turnaround working, and could Nutanix actually make it into profit?

Background

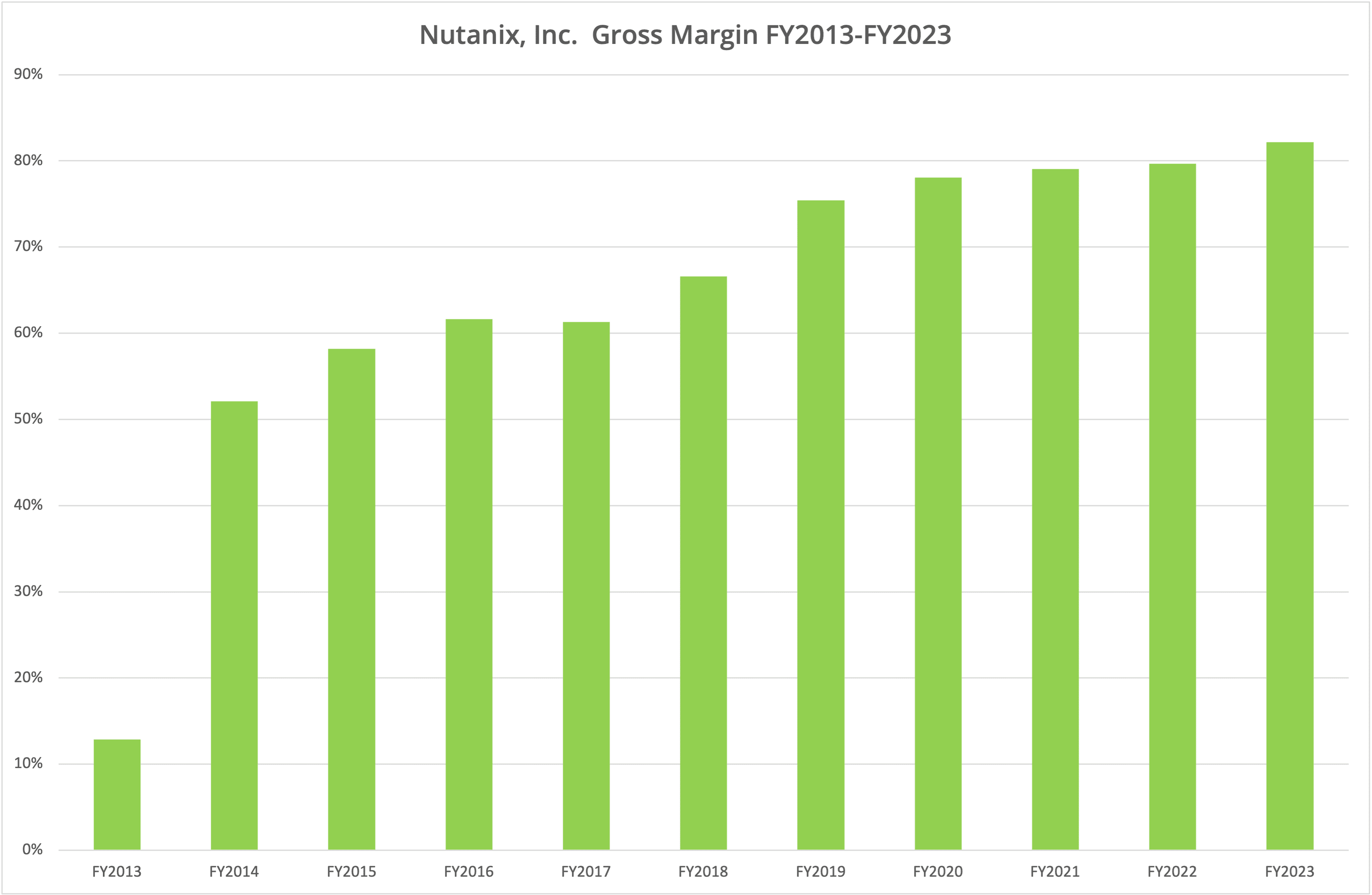

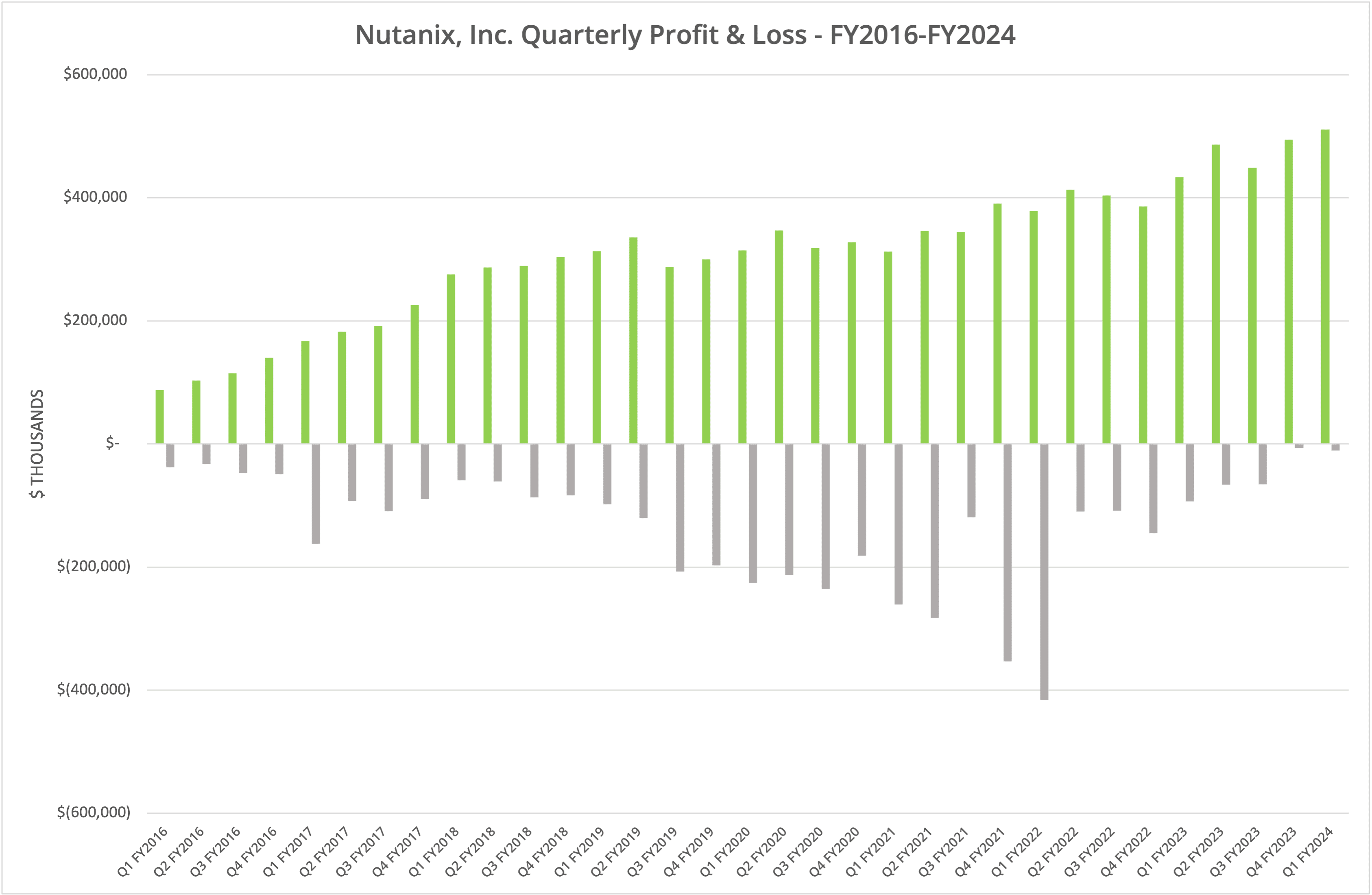

Nutanix, Inc. has published financial data for Q1 FY2024. Revenue was $511 million, up 17.8% on Q1 FY2023 and 3.4% sequentially. Gross margin continues to climb, at 84% in the current and last reporting periods. However, overheads increased slightly to $435 million (up 1% year-on-year and 2.3% sequentially). This resulted in a loss of $11 million for the reported period.

Nutanix claims to have acquired 24,930 customers, an increase of 380 over the previous quarter. Annual recurring revenue (ARR) is up 30% year-on-year at $1.664 billion.

Growth

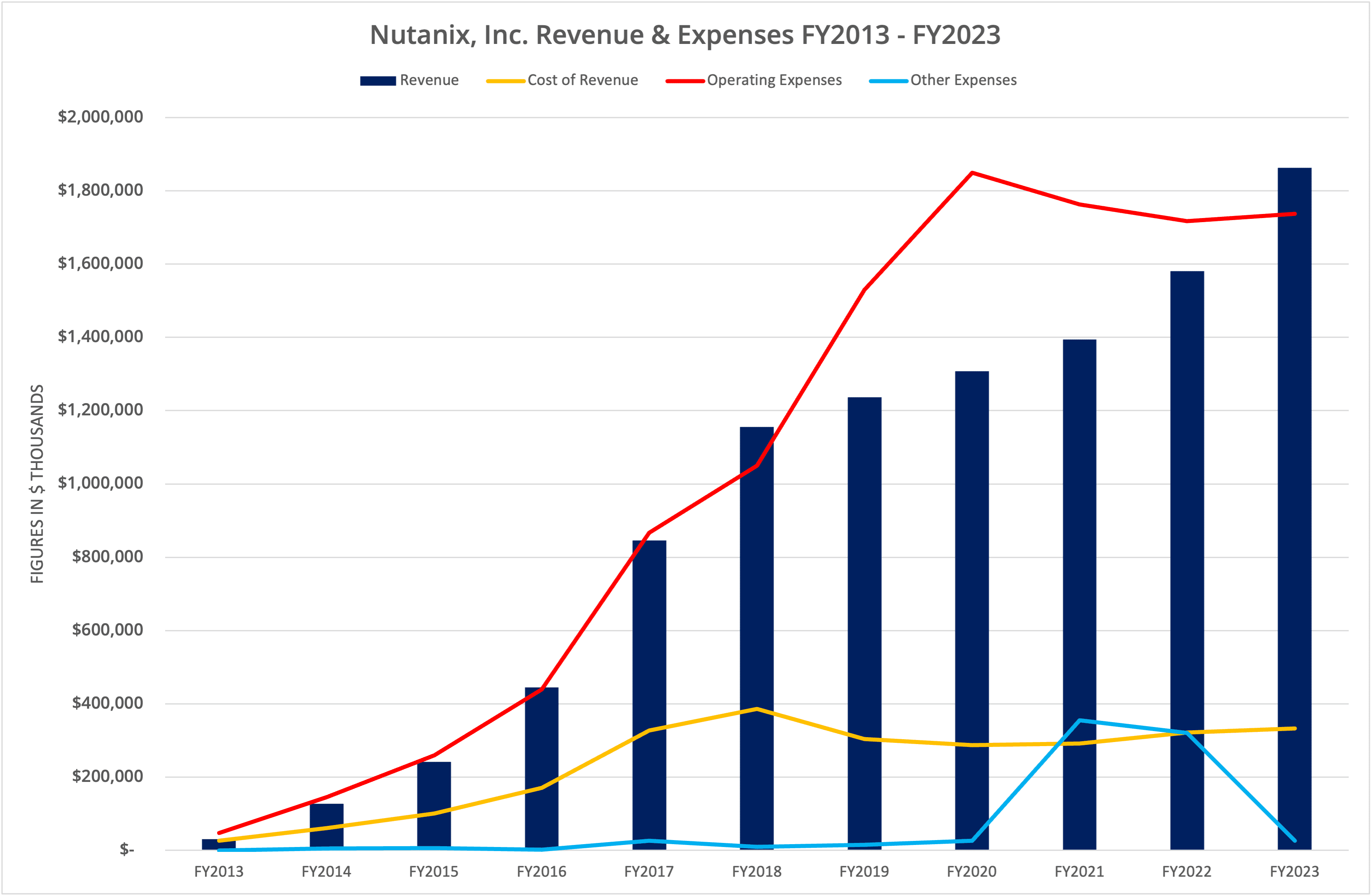

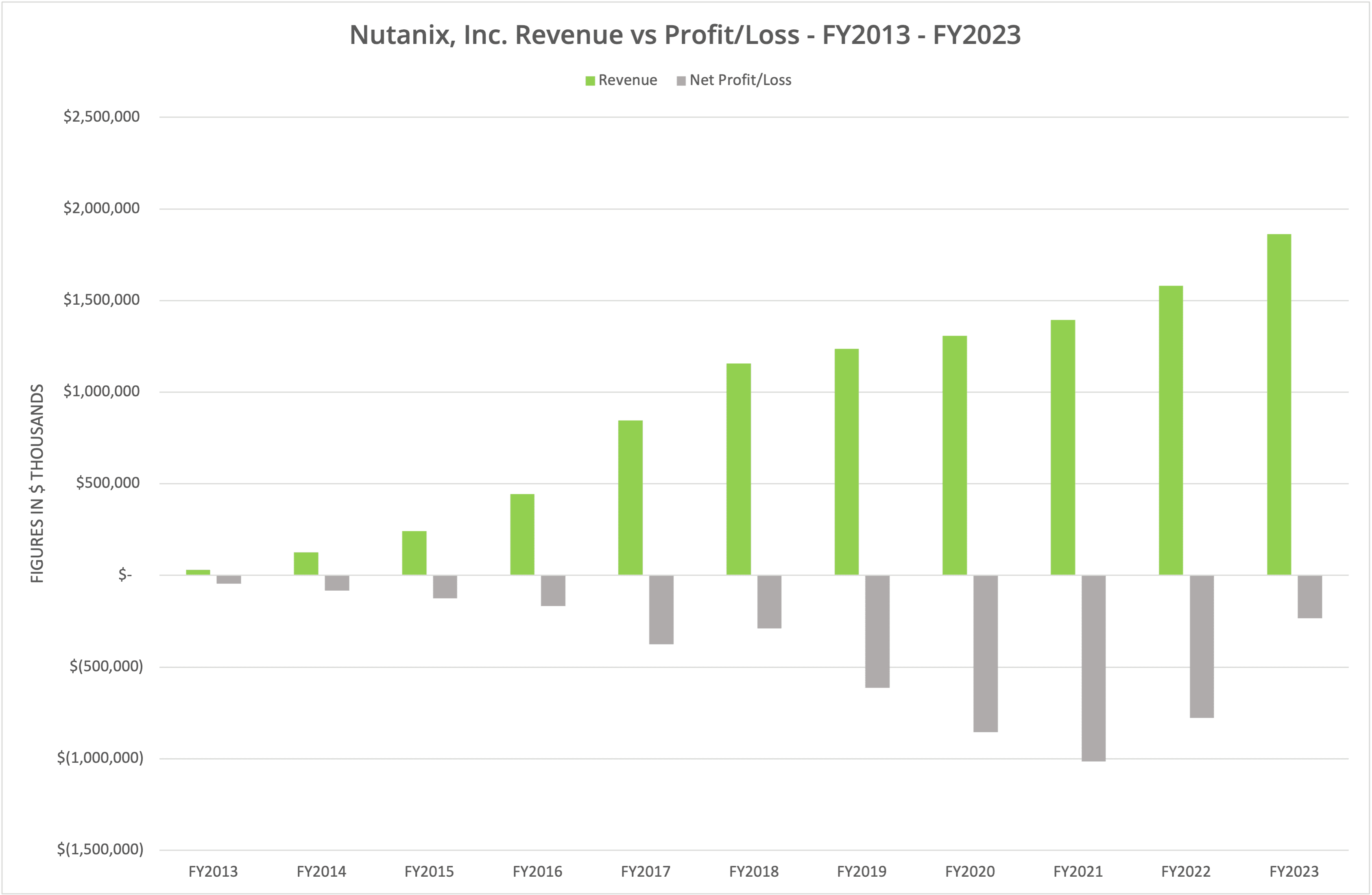

Nutanix has been a growth business since its inception, with revenue increasing every year in the periods for which data is available (FY2013 – FY2023, Figure 2). However, until FY2021, expenses and subsequent losses increased in equal measure. In December 2020, Rajiv Ramaswami was appointed CEO, and since then, we’ve seen a stemming and decline in losses to the level where Nutanix could be classed as an almost break-even business.

Inflection Point

In the current market, there is much uncertainty for the future direction of VMware, with the acquisition of Broadcom now completed. Many news articles have claimed up to 20% of the VMware customer base could move elsewhere, representing a significant opportunity for Nutanix to gain business.

To make this transition work, Nutanix must convince prospective customers to migrate to AHV, the native Nutanix hypervisor. Currently, around 50% of Nutanix customers still use VMware vSphere, with this figure static for several years. VMware did such a good job building a reliable type-1 hypervisor that many customers may be reluctant to move elsewhere, representing a challenge for Nutanix (and many other virtualisation vendors).

Ecosystem

From Nutanix’s perspective, the company has arguably the most mature ecosystem of any virtualisation vendor except VMware. Moving from VMware to the Nutanix ecosystem is relatively easy, depending on the level of integration (scripts, processes) that would need rewriting. So, the company is in a strong position as we look forward to calendar year 2024.

Expenses

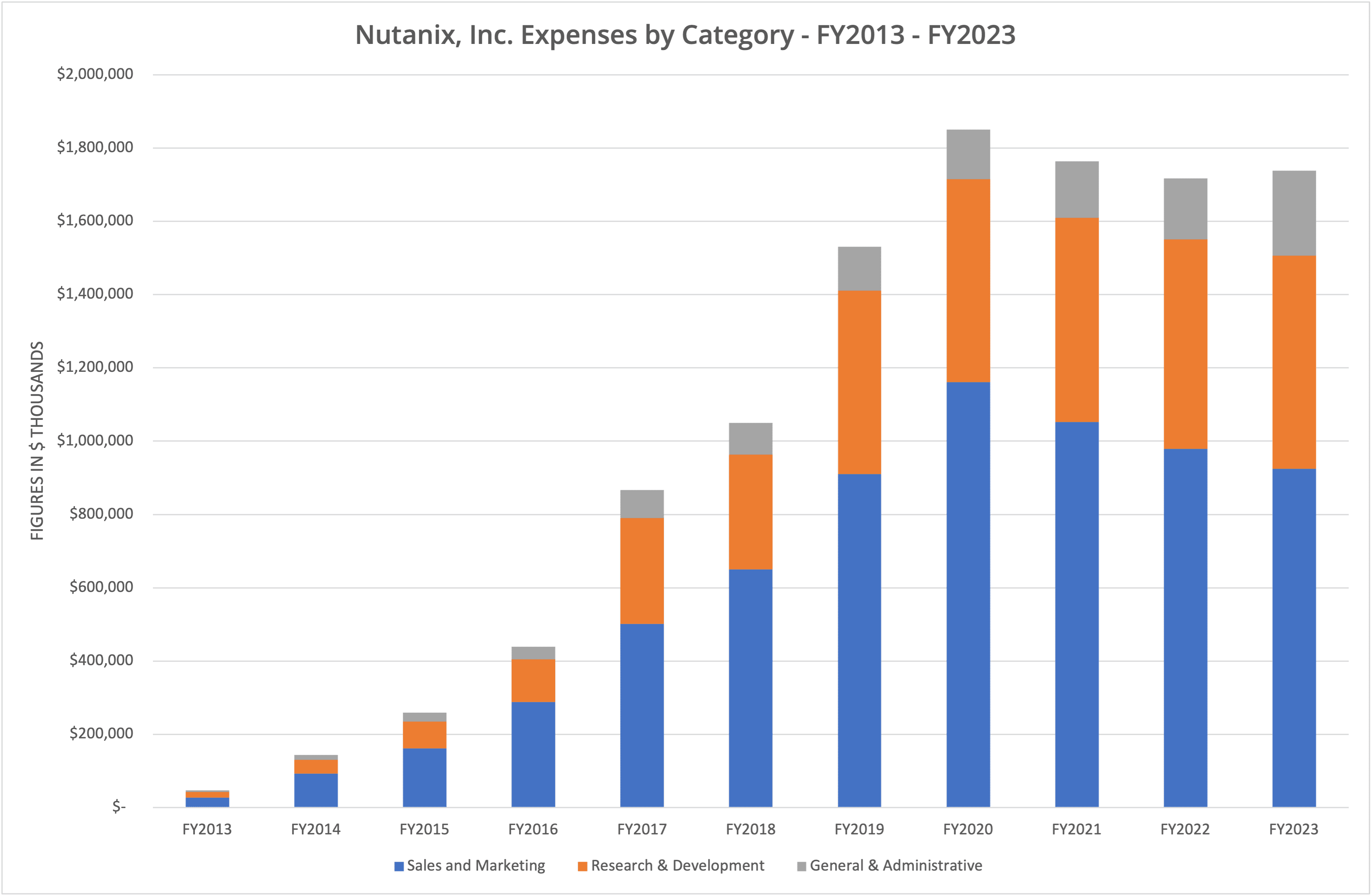

The only issue, financially, is the expenses challenge. If those numbers can be brought down, then Nutanix can quickly reach profitable status. Relatively speaking, the R&D budget is high and must be capable of trimming. In addition, the sales and marketing figures should represent an opportunity for optimisation.

We think this is possible because the VMware acquisition will naturally create significant disturbance in the market. Nutanix needs to convince ex-VMware customers to remain on-premises rather than consider a pivot to the public cloud.

The Architect’s View®

The focus on expense reduction at Nutanix is impressive but needs to go further. With such a massive opportunity to gain market share, Nutanix needs to capitalise on the “fear, uncertainty and doubt” introduced by the VMware acquisition. With further expenses controls in place, Nutanix could finally be a profitable company and grow to rival the success of its most significant competitor, VMware.

Copyright (c) 2007-2023 – Post #bcc4 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.

This post is only available to Individual, Vendor or Enterprise subscribers. Restrictions on distribution are based on those licensing terms. Check our Terms of Service for details.