Veeam Software has appointed a new CEO and set an ambitious $10 billion revenue target and the possibility of IPO. How achievable is this financial goal in a highly competitive market that is quickly adopting SaaS-based data protection?

Update: This post has been updated details from Veeam’s 25th January 2022 press release.

Background

Veeam Software was founded in 2006 by Andrei Baronov and Ratmir Timashev. The company has evolved from virtual infrastructure monitoring products to produce data protection for small, medium and enterprise customers. After years of self-funding, the company took an undisclosed amount of money from Insight Partners in 2013, followed by a further $500 million in 2019. In March 2020, Insight Partners acquired Veeam for $5 billion.

SME

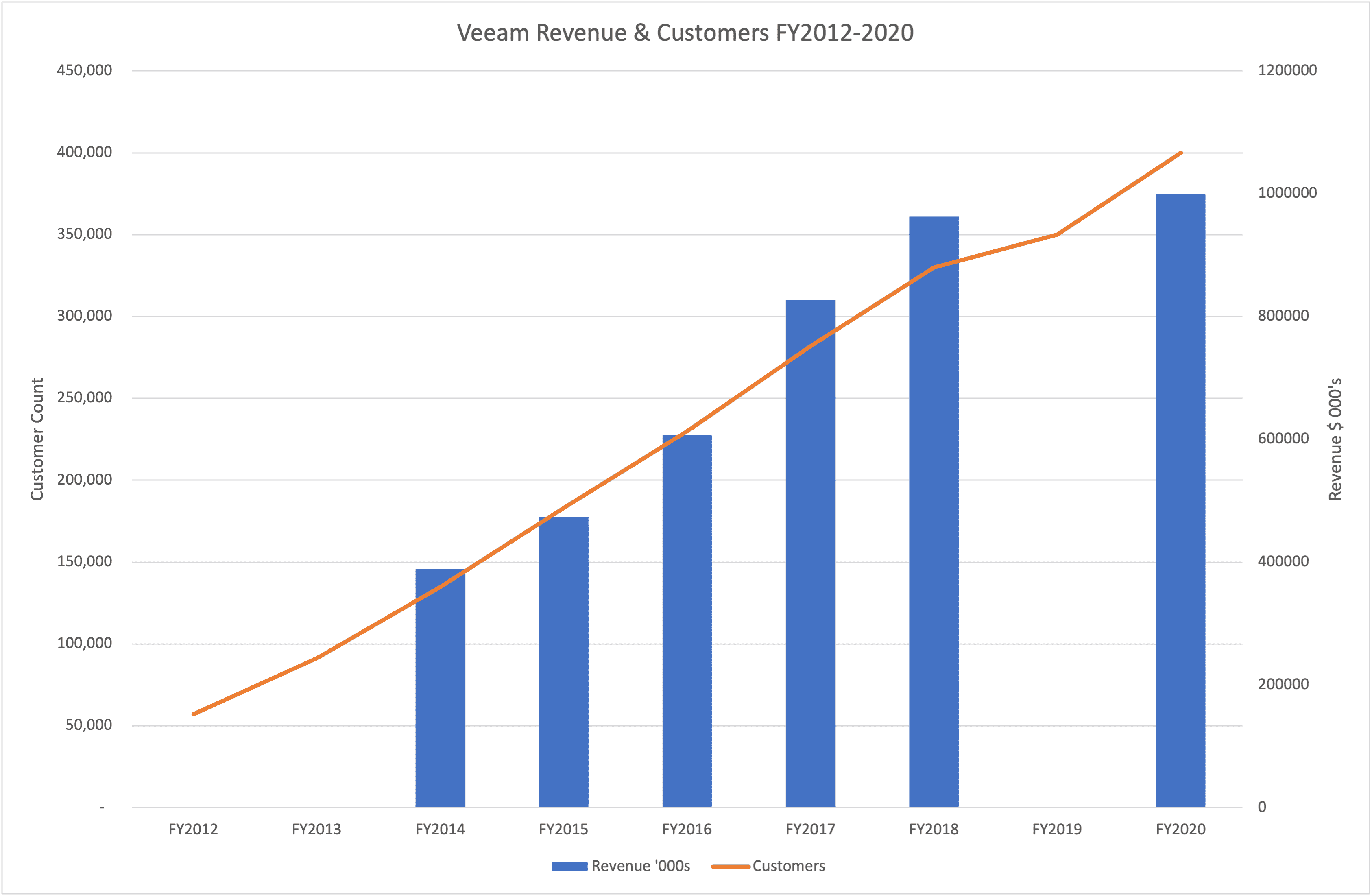

Veeam has been on a constant upwards trajectory of revenue and increasing customer numbers. As the company has always remained in private hands, there’s no requirement for external reporting. However, we’ve pieced together some revenue and customer numbers from FY2012 onwards. The data is shown in table 1, with the source for this information coming from Veeam press releases.

| Period | Revenue (000s) | Customers | Revenue/Customer |

| FY2012 | No data | 57,000 | |

| FY2013 | No data | 91,500 | |

| FY2014 | $389,000 | 135,000 | $2881.48 |

| FY2015 | $474,000 | 183,000 | $2590.16 |

| FY2016 | $607,000 | 230,000 | $2639.13 |

| FY2017 | $827,000 | 282,000 | $2932.62 |

| FY2018 | $963,000 | 330,000 | $2918.18 |

| FY2019 | No data | 350,000 | No data |

| FY2020 | $1,000,000 | 400,000 | $2500.00 |

| FY2021 | No data | 400,000+ | No data |

Veeam didn’t start reporting specific revenue numbers until FY2014 (using previous period percentages instead), although customer figures are available from FY2012 onwards. We can’t find any FY2019 financials announcement other than a statement on customer numbers (so this could have been a down year). Through the timeline, reporting terminology has included revenue, bookings and ARR, which we’ve assumed to represent the same number. We realise that ARR isn’t the same as perpetual revenue and maintenance, but with no other data to use, we’ve assumed they’re the same (more on this in a moment). The latest reporting indicates an ARR of “greater than” $1 billion, so we’ve left that at $1b for FY2020.

If we divide revenue/ARR by customer count, we can see a remarkably consistent revenue per customer ratio. This value is between $2500 and $3000 per customer per year. This figure equates to a Veeam Universal Licence for around only 30 virtual machines (source: Veeam pricing calculator). The calculation doesn’t include any margin for resellers, so the actual figure is likely lower. Of course, we’re using averages here and not taking into account large enterprise subscriptions, which could make this average figure even lower.

The difference between revenue, ARR and bookings in the Veeam context is an interesting one. It appears that different numbers are used over time as a transition to ARR occurs. However, as this recent article from Chris Mellor shows, Veeam’s revenue for the second half of 2021 as $647 million, putting annual revenue on target for around $1.2 billion and on the trend of previous years. Of course, as a private company, these numbers aren’t publicly available or verifiable.

Growth

Veeam growth numbers look consistent and have hovered around 50,000 per annum for the last 5-6 years. Assuming a continuing static customer revenue ratio, Veeam would need to reach around 4 million customers to see ARR of $10 billion. That’s roughly 72 years at the current growth rate. This clearly isn’t a practical route to significant revenue. So, the alternative is to make more money from existing customers – or move into new markets.

Squeeze

How practical would it be for Veeam to extract more from each customer? We don’t know the size distribution across the continuum of the 400,000 customers, but in reality, a large proportion of those must be small or medium enterprises. Making additional revenue from businesses that don’t have a need (or ability) to spend more on data protection is a challenging prospect.

If we look at VMware by way of comparison, the company claims approximately 500,000 customers, with revenues of around $11 billion. Can Veeam turn their data protection business into one to rival VMware in terms of scale and income?

Let’s dig into the Veeam software solutions and see what could be achieved.

Portfolio

The Veeam software portfolio is currently based around two products. Veeam Backup & Replication offers data protection capabilities for on-premises, SaaS and public cloud workloads. Veeam ONE delivers unified monitoring and reporting across all customer’s data resources. The design of these solutions is implemented with many point products that protect specific data types, including K10, from the acquisition of Kasten in October 2020.

Support for public cloud workloads is implemented through products that run as virtual instances within the public cloud. These include Veeam Backup for AWS, Veeam Backup for Microsoft Azure and Veeam Backup for Google Cloud Platform. Alternatively, customers can make backup copies to on-premises infrastructure running Veeam Backup & Replication.

The Veeam cloud story is less developed than other vendors. The company currently has no in-house SaaS offering, relying instead on partners to deliver this capability. Cloud workloads are supported through virtual instances running in the customer’s account and using customer-supplied storage buckets. This model represents both a ransomware risk and a challenge for data mobility between public cloud providers.

Evolution

Two major portfolio challenges leap out of this analysis. First, Veeam needs a stronger SaaS story, including with respect to the public cloud. Looking at the broader market, HYCU, Metallic (Commvault), Druva, and Clumio already have native public cloud data protection solutions. We’ve previously highlighted HYCU, which offers support across all three major cloud platforms (Azure, AWS, GCP) and on-premises infrastructure with a consistent look and feel as well as data mobility. Druva, Metallic, and Clumio are solutions built natively using public cloud services, so offer instant scale-up/down for the vendor and aid the rapid onboarding of new customers, as well as maintaining resource efficiency. Veeam doesn’t have this flexibility with the legacy virtual instance model.

The second challenge is the need to address the long-term requirements of hybrid and multi-cloud. Today, Veeam offers a collection of solutions that have different interfaces and back-end data storage methods. This strategy isn’t a problem for small and medium customers but represents a significant challenge for larger enterprises, where scale requires standardisation. As enterprises continue to increase their cloud diversity, standardisation of data formats and cross-platform, as well as cross-cloud interoperability, will be essential. This direction also means standardising management portals and tools.

The Architect’s View™

We can see four scenarios for Veeam’s future, all of which could play a part in the ongoing direction of the company.

- Continued Growth – this option is pretty much a given; Veeam will continue to acquire new customers, but with no guarantee of how quickly that growth will occur or ramp up.

- Portfolio Review – design and build solutions that are, by nature, enterprise-capable and hybrid/multi-cloud ready. This strategy risks creating the implication that existing products aren’t enterprise-capable, even as enterprise customers use the current product set today.

- Acquire – buy in the technology to go after the enterprise, including the acquisition of higher value customers. Kasten represents one area of increased diversity, but this market is unproven in the long term. Buying out competitors might be out of reach for Veeam, as valuations for data protection companies are high.

- New Markets – Veeam could enter entirely new markets, tapping the growth in AI and analytics as one example. This route would probably require acquisition to gain a quick foothold and could take a few years to be significant to revenue numbers.

So, lots of possible choices are available, with no single direction likely.

The data protection market has seen massive expansion over the last decade, with billions of dollars of investment. We believe that the number of vendors competing today has reached close to saturation point, with many gaining market share at the expense of legacy providers.

In parallel, the rapid transition to the public cloud has transformed the perception of data protection into just another service to be offered alongside storage, networking, and compute.

Data protection is a long-term game, as backups are generally not portable and must be retained for timespans measured in years. As a result, customers have inertia to change between providers.

Veeam has a new CEO who needs to articulate what future strategies will enable the jump of revenue ten-fold. Anand Eswaran has a lot to deliver in the next 15 years of the Veeam story.

Update: 26 January 2022. Veeam published a press release on 25 January 2022, with an update on FY2021 trading. ARR grew 27% year-on-year, although we don’t know what percentage of overall revenue ARR contributes to the bottom line. Individual product growth is quoted for a mix of products, specifically the cloud and SaaS offerings, which would be expected to grow quickly at this point.

The most challenging figure is the quote on 16 quarters of double-digit growth. This figure is, at a minimum, 10% per quarter, which equates to 46% per annum, or 460% over 16 quarters (4 years). With a quoted figure of $827,000 four years ago, this means Veeam’s revenue should be in the region of at least $4 billion on the lowest estimate, which clearly, based on data from IDC, is not the case.

Further information on the data protection market is available in our premium eBook, Essential Capabilities for Modern Data Protection, available to buy and download today at $495.

Further Reading

- Kubernetes data protection – container-integrated or separate backup?

- Clumio Introduces Data Protection for S3

- HYCU Introduces Protege Data Protection for Kubernetes

- Data Protection for Heterogeneous Environments

- Commvault Announces Metallic Saas Data Protection

Copyright (c) 2007-2022 – Post #3567 – Brookend Ltd, first published on https://www.architecting.it/blog, do not reproduce without permission.